We use essential cookies to make our website work properly when you visit us. We’d also like your consent to set other non-essential cookies to help us improve our website and tailor the marketing you see.

A lifetime mortgage is a loan secured against your home. There are typically no monthly repayments to make with a standard lifetime mortgage as the loan, plus roll up interest, is typically repaid through the sale of the property when the last remaining applicant passes away or moves into long term-care.

Instead, the interest is added to the loan which rolls up and compounds over time, meaning the amount you owe can grow quickly.

How compound interest works

Compound interest means you pay interest on both the original amount you borrowed and on any interest that has already been added. Each month or year, the interest is added to your loan balance, and then new interest is charged on this updated balance. If you don't make voluntary payments, the balance will grow quickly over time.

However, with all our plans, you can choose to make voluntary repayments without incurring an early repayment charge (subject to criteria).

Equity release may leave you with limited or no property equity remaining and will reduce your financial options in the future.

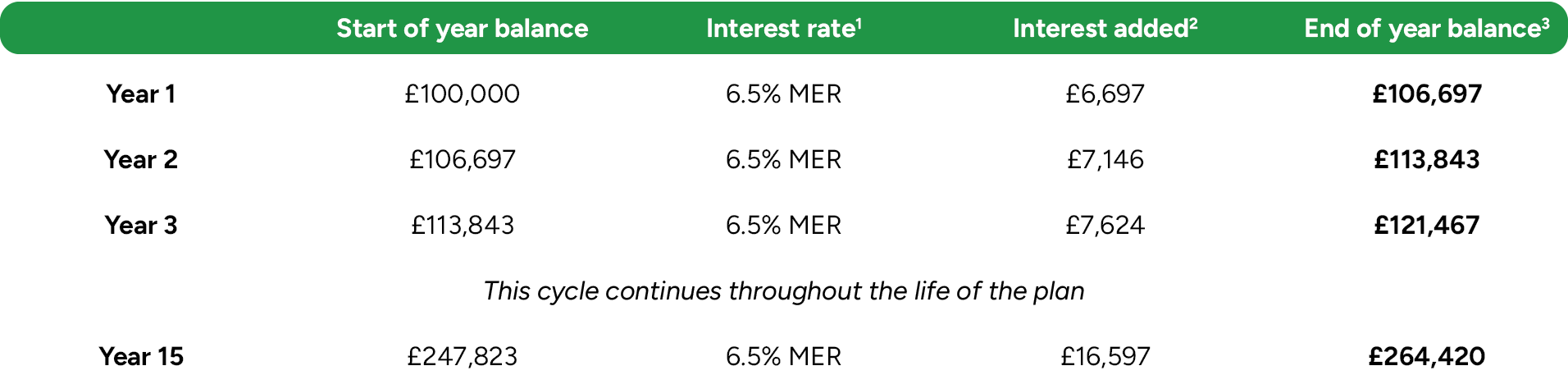

Initial release amount of £100,000. Plan subject to a fixed interest rate of 6.5% MER (Monthly Equivalent Rate)

1. The interest rate is fixed for life on all more2Iife lifetime mortgages.

2. Interest is charged on the balance at the start of the year, not the original loan amount.

3. The balance at the end of the year, including compound interest.

Equity release will reduce the value of your estate and may affect your entitlement to means-tested benefits.

All our plans come with the option to make ad-hoc or regular repayments to help reduce your total cost of borrowing. Usually, you can only repay a portion of your initial loan (10-15% depending on your plan) within each 12-month period without incurring an early repayment charge (ERC). That's until your ERC period ends.

Alongside helping you manage borrowing costs, some of our plans offer an Interest Reward feature, rewarding you with a discounted interest rate in return for making monthly payments.

Learn more >

For example, our Apex Interest Reward Lifetime Mortgage - available to homeowners aged 55-84 - rewards you with an interest rate discount of up to 0.75% for committing to make monthly payments for 15 years. You'll always retain full ownership of your home with our Apex Interest Reward plan, even if you stop making payments early. Once you reach the end of the payment period or if you stop making your monthly payments sooner, this lifetime mortgage will convert to full interest roll-up and the interest rate discount will be removed.

If an Interest Reward option isn't the right option for you, you're still able to make repayments towards a regular lifetime mortgage, subject to criteria, it’ll help reduce the amount of interest you pay over the lifetime of your loan. These are long-term financial products and are not designed to be repaid early. If you do, early repayment charges may apply

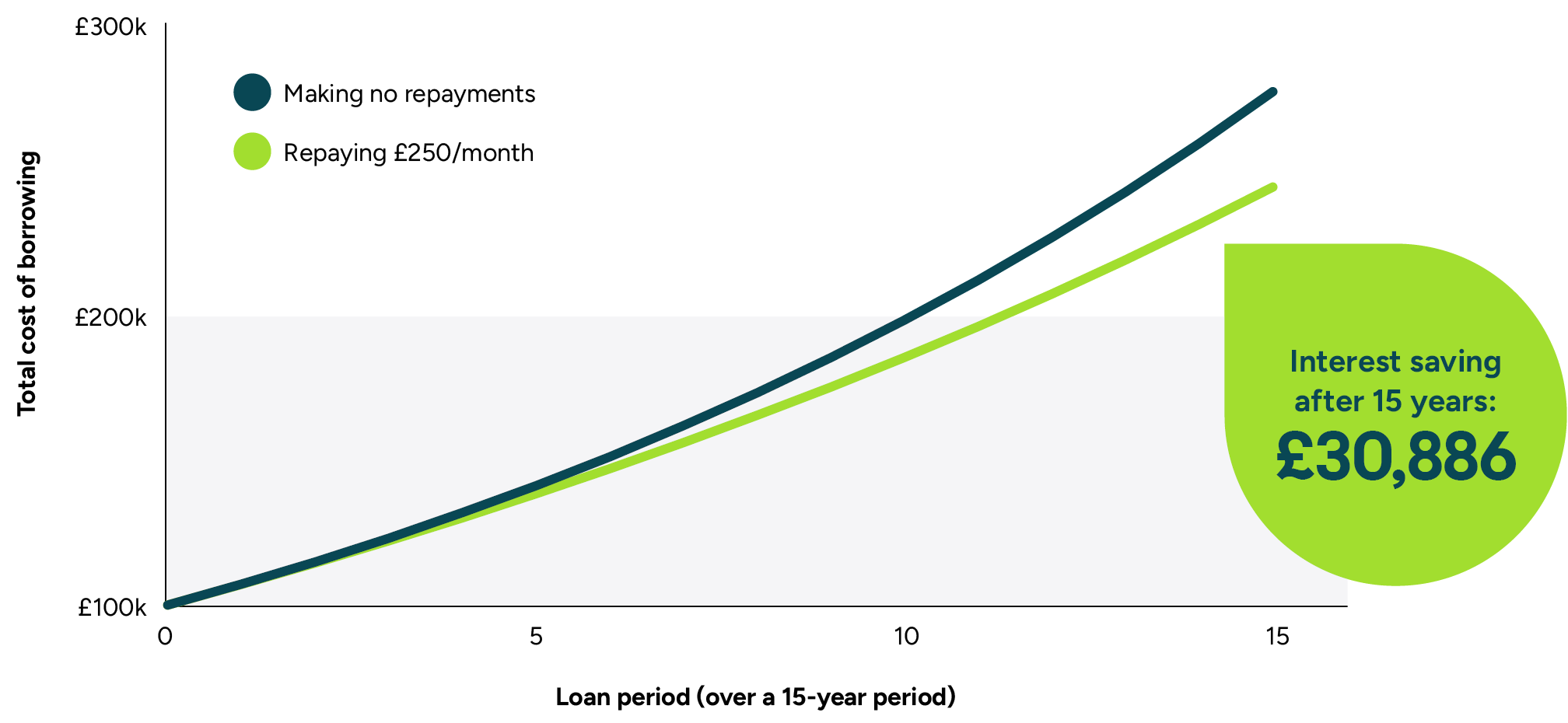

Initial release amount of £100,000. Plan subject to a fixed interest rate of 6.5% MER (Monthly Equivalent Rate).

Interest and repayments shown over a 15-year period.

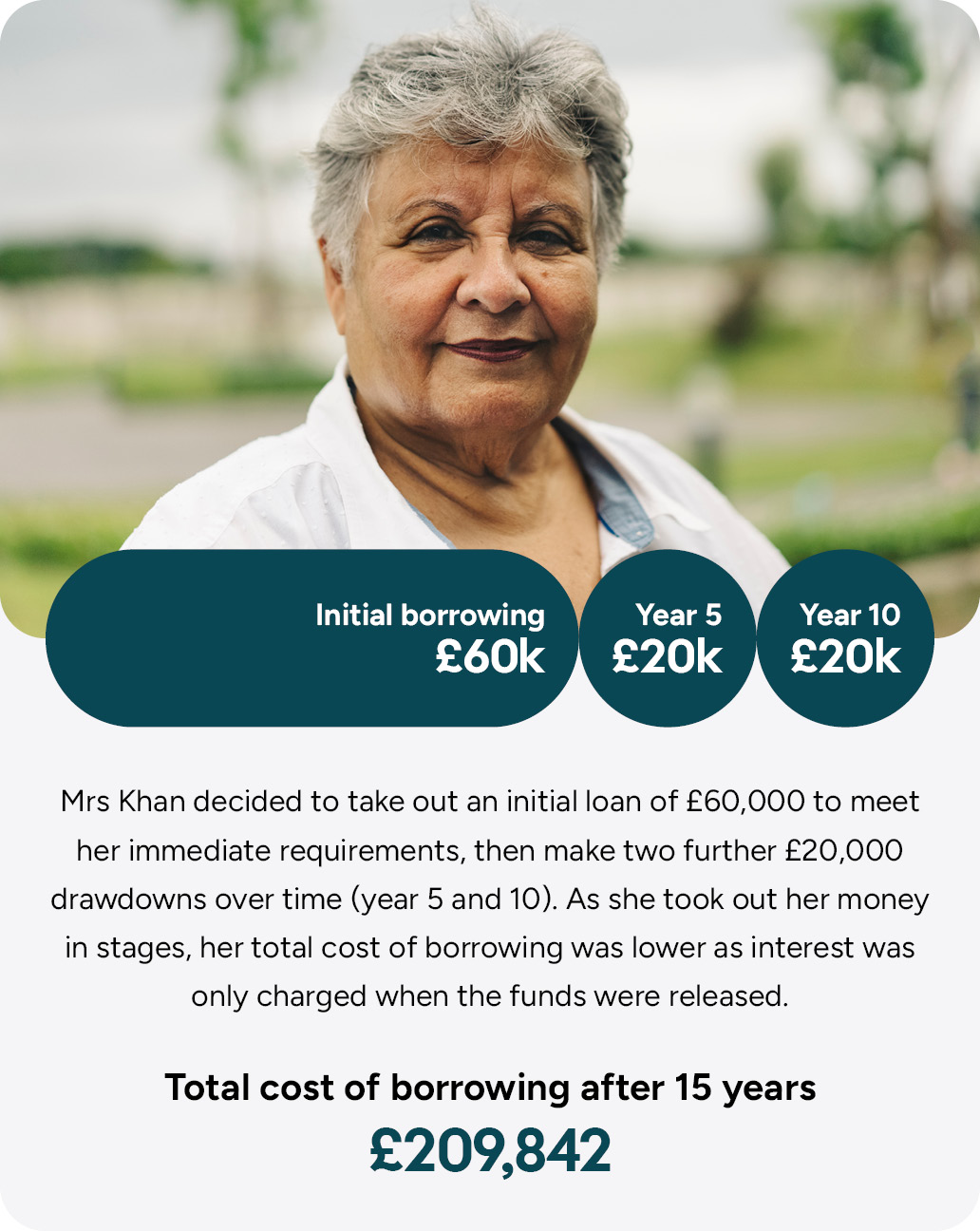

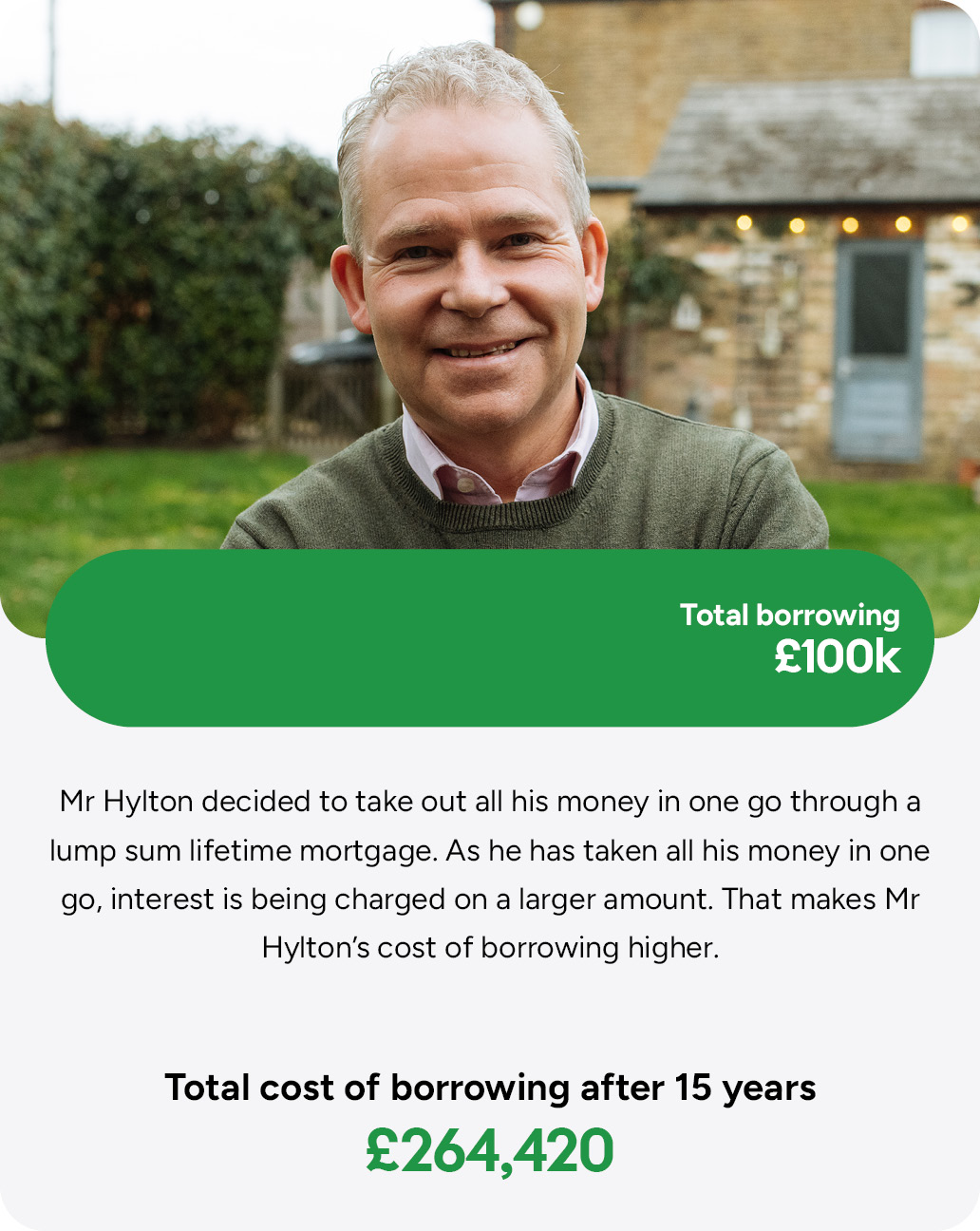

With a drawdown lifetime mortgage, you only take out the money you need when you need it, following an initial release. This can help reduce your total cost of borrowing, as interest is only charged on the money you release, rather than the full amount available. It’s worth noting, however, that drawdowns aren”t guaranteed. If you choose to make a drawdown, the funds will be at the prevailing fixed interest rate at the time. This new rate may differ from your original interest rate.

Learn more >

Mrs Khan and Mr Hylton both want to release £100,000, but opted

to take it out in different ways to meet their requirements. Mrs Khan

chose drawdown, while Mr Hylton chose lump sum.

This example is for illustrative purposes only and uses the monthly equivalent rate of 6.5% throughout. Important note: drawdowns

will be charged at the prevailing interest rate at the time of release, which could be higher or lower than the initial interest rate.

If interest rates reduce in the future, you may have the option to remortgage your current plan to secure a lower rate. By paying a lower interest rate, you can reduce your total cost of borrowing. However, a reduction to interest rates in the future isn’t guaranteed.

It’s also important to remember that there may be an early repayment charge (ERC) payable if you choose to remortgage your equity release plan. However, most modern lifetime mortgages come with fixed ERCs.

At more2life, most of our plans come with fixed ERCs which expire after a certain amount of time. We even offer a plan with no ERCs if this plan is most suitable for your needs. Your adviser can explain this in more detail to you.